You know credit scores exist. You might even know what yours is. But do you know how it's calculated and why it's important?

Your credit score affects whether you can get a credit card, rent an apartment, buy a house, start a business, or even get a cell phone contract.

A low credit score can limit your choice of loans or determine if you can get one at all — and if you can, it might have a high interest rate.

“There’s a huge cost to having a low credit score that happens to people, an actual true financial cost to them, and it’s a shame that people don’t learn about this or know about it or pay attention to it until usually it’s too late,” said Colleen McCreary, consumer financial advocate at Credit Karma.

Here's a look at how you can create healthy habits to avoid having a low credit score:

What is a credit score?

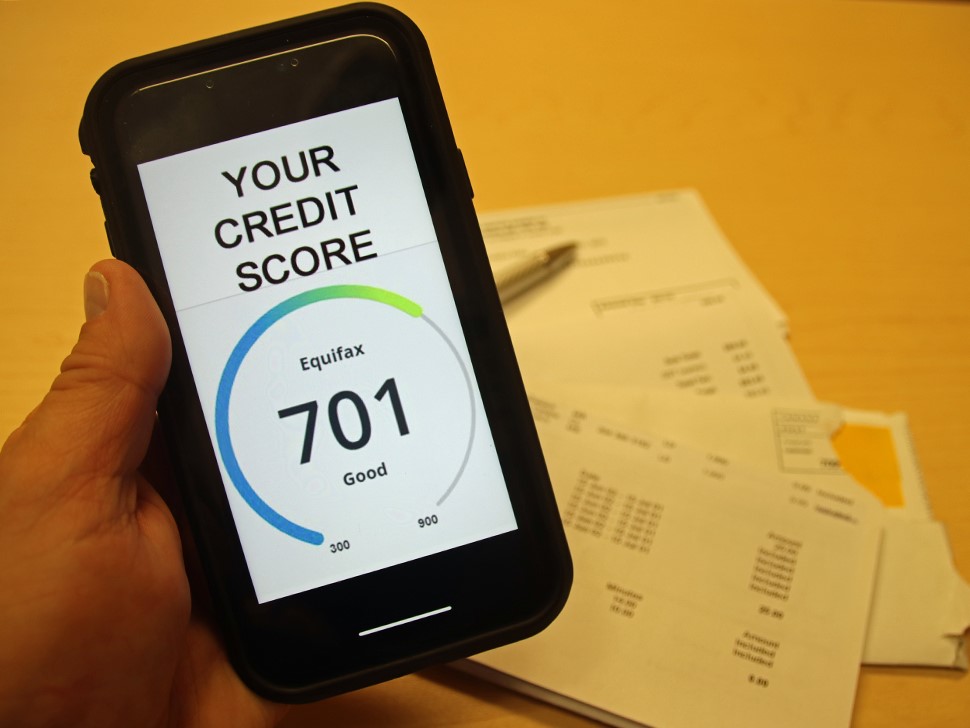

A credit score is a mathematical formula that helps lenders determine how likely you are to pay back a loan. Credit scores are based on your credit history and range from 300 to 850.

“It’s a score that is going to determine how comfortable people are to lend you money,” McCreary said.

If your credit score is high, you can borrow more money. But if it’s low, you can borrow less or no money, or borrow money with a high interest rate, which can then create more debt.

Banks, landlords and insurance companies look at your credit score to determine the type of credit card that you can get approved for, whether you are the right fit for an apartment, and your insurance rate, among other things.

"Essentially, the bank will say 'Hey, you don’t have a great credit score. Instead of a 2% interest rate, we’re going to give you a 3% interest rate,'" said Kristin Myers, editor in chief of The Balance, a personal finance website. "It might mean that you’re paying out more money over the lifetime of a loan every single month.”

https://www.canada.ca/en/financial-consumer-agency/services/credit-reports-score.html

How is my credit score calculated?

While the idea of credit scores is simple, the way they’re determined is more complicated.

Credit scores can come from several credit reporting agencies. You can access your credit report online for free from Equifax and TransUnion. Each has its own model to calculate credit scores.

While we know generally what factors into the credit scores, the agencies don't share their specific formulas with the public. But each produces a slightly different score.

“One is scoring like a basketball game, one is like a football game and one is scoring like a hockey game,” said McCreary, who added that you shouldn’t worry if one agency gives you a few points less than others.

Since you don’t know which agency your lender is going to use to check your credit score, McCreary also recommends that you check all three of them before requesting a large amount of credit.

Here are the factors that are frequently used to calculate your credit score:

- Bill payment history

- Length of credit history

- Current unpaid debt

- How much of your available credit you’re using

- New credit requests

- If you have had debt sent to collection, foreclosure, or a bankruptcy

One thing that doesn’t affect your credit score is how much money you make, said McCreary. But you still need to take care to only borrow the amount you can afford to pay back.

Other aspects that don’t affect your credit score include your age, where you live and your demographic information such as race, ethnicity, and gender, according to Experian.

How do I find out my credit score for free?

There are several ways that you can check your credit score for free. A great place to start is to check if your bank offers this service for its customers. Additionally, each of the credit reporting agencies allows you to check your credit score for free.

What is a good credit score?

You are considered to have a good credit score if it’s 670 or higher. If your credit score is over 750, you’re considered to have a great credit score, said McCreary.

“There is this sort of dream scenario of having an over 800 credit score, that is a very high credit score and very few people get there,” said McCreary.

“Fair” credit scores are considered to be in the 580-669 range, a credit score below 580 is considered a poor credit score.

Six tips for improving your credit score

The journey to improve your credit score is different for everyone. But some steps that can help you tackle credit card debt include paying at least the minimum monthly payment and, if you can, paying just a bit more over the minimum so you pay less interest over time.

1: Know your starting point

The first step towards increasing your credit score is knowing your current score and what is showing in your credit report, said Kristin Myers, editor in chief of The Balance a personal finance website.

“You can’t fix what you don’t know,” she said. “See if there are any errors or if you’ve previously made a dispute and it keeps showing up.”

Once you see what is in your report, you can start identifying where you might have weaknesses. For example, if you have a large amount of debt on one of your credit cards, start paying off that debt to reduce the credit utilization that is affecting your credit score.

2: Tackle your debt, as much as you can

Ideally, you pay off your credit card every month. But, if that is not possible for you, making small payments can help you maintain or increase your credit score.

If you can, pay just a bit more over the minimum monthly payment so you pay less interest over time.

A well-known payment method is the “debt snowball” where you pay down your debts from smallest to largest, to build momentum and good habits. Once the smaller debts are paid off and you have built a habit of paying off debt, the money you were used to putting aside every month can then go toward larger debts.

3: Avoid more debt, if you can

Not acquiring new debt is another way to increase your credit score, Myers said. If you have not paid off the debt that you currently have, it’s best to not open more lines of credit. If you are in a position where you rely on credit due to economic circumstances, try to avoid unnecessary purchases that could significantly increase your debt.

4: Use credit cards, but in moderation

Many people’s first instinct is to not use any credit cards to avoid getting into debt. However, this is not a good tactic if you want to have a good credit score. It’s best to have at least one credit card but the key is to use it moderately, said Colleen McCreary, consumer financial advocate at Credit Karma.

“You don’t want to use more than 30 per cent of the credit that’s available to you, but you want to be using those cards even just a little bit to prove that you can be trusted,” she said.

When using your credit card, make sure to pay on time each month and try to use it only for purchases that you were already planning to make, and can afford.

5: Do not close your old accounts

After you have paid off your credit card, you might think it’s best to close the account to avoid using it again.

This actually hurts your credit score. Since one of the factors in your credit score is the length of your credit history, if you close your oldest credit card account, you are also erasing this from your credit history.

“Keeping the length of that credit history open is incredibly important because the length of time you’ve had a loan or line of credit is going to boost your credit score,” Myers said.

6: If you don't have any credit history, start safe

If you are starting and want to build your credit, there are several ways to make this process safe for you to not get into debt. One of the most recommended ways is to open a “secured card,” which are credit cards that require a deposit that usually amounts to the amount of credit that you are given.

The deposit is there in case you can’t pay back the credit but it is given back to you after you upgrade to an “unsecured” card. Secured cards are reported to the credit bureaus, which means this line of credit shows in your credit report and it can help build or fix your credit score.

The Government of Canada provides resources on how to improve your credit score as well.

Does checking my credit score lower it?

Checking your credit score does not lower it unless you are making a “hard inquiry,” which is only done when requesting a line of credit.

Soft inquiries, where you want to know your credit score, do not affect your score and it’s a good habit to check your credit score often to make sure it’s accurate.

On the other hand, lenders make hard inquiries when you apply for credit like a mortgage or a car loan, and those do show up on your credit report.

McCreary recommends not making several requests for credit at the same time since this could hurt your credit score. It’s best to know beforehand what your credit score is and then apply when you are confident that your loan will get approved.

How can I create healthy habits with my credit score?

The first step is to check at least once a year to make sure you are comfortable with your current credit score.

If you are planning to request a large credit line, you want to check your score a few months prior and see how you can start improving it. If you are currently trying to increase your credit score, it’s recommended that you check it often to see if your actions are making a difference.

If you notice a mistake in your credit report, you can dispute it by contacting the respective credit reporting agencies.

Being aware of your credit score and maintaining healthy habits around it is crucial to having a good credit history. However, it is important for people to know that their financial worth shouldn’t be attached to their credit score, Myers said.

“It doesn’t mean that you’re a bad person or terrible with money and that you need to constantly beat yourself up,” she said.

Fri, Jul 26, 6:00 PM

Fri, Jul 26, 6:00 PM

Full-time, Permanent, Labour

Full-time, Permanent, Labour